- Madrid’s miracle: Spain’s VAT cut on fuel, electricity, and gas drove inflation down from 3.4 to 3.2 per cent in April while peers climbed.

- Berlin follows suit: Germany’s parliament approved a temporary cut to the mineral oil tax for May and June, defying its own Council of Economic Experts.

- The 80 per cent rule: Evidence from the 2022 Tank-Rabatt shows roughly four-fifths of the rebate reached drivers, contradicting claims of futility.

- The central bank dilemma: Temporary energy subsidies relieve the European Central Bank of an impossible choice between inflation credibility and recession risk.

- A continental answer to Trump: As Washington’s tariff offensive and Middle East brinkmanship destabilise energy markets, a coordinated European fiscal response becomes essential.

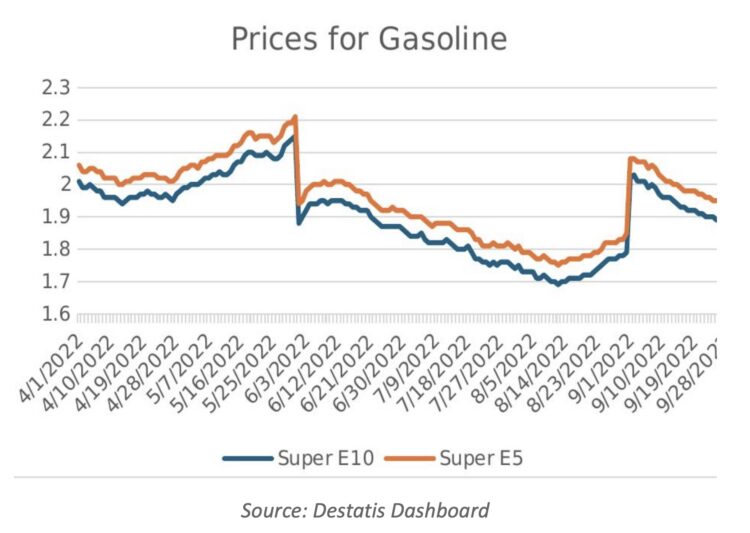

Inflation rose across the major economies of the European Union (EU) in April 2026 as global energy prices climbed. Spain stood apart. The Spanish rate fell from 3.4 per cent in March to 3.2 per cent in April. What explains the miracle? On 20 March 2026, the Madrid government cut value added tax (VAT) on fuel, electricity, and gas from 21 per cent to 10 per cent, lowered the tax on hydrocarbons to the minimum permitted under EU rules, and introduced tax credits and aid for the sectors hardest hit by the consequences of the war in Iran.

In Germany, on 24 April, the Bundestag adopted a similar measure—a fuel discount, or Tank-Rabatt, suspending most of the mineral oil tax during May and June 2026.

These improvisations come at a moment when Europe is contending with a wider economic disorder. Donald Trump’s second-term tariff offensive and his confrontational posture in the Middle East have intensified the supply-side pressures bearing down on European households. The question facing governments is no longer whether to act, but how.

Government subsidies to dampen energy price increases have a poor reputation among economists. In Germany, Monika Schnitzer, the chairwoman of the German Council of Economic Experts, described the measure as “the worst of all options considered thus far”. Alfred Kammer, the director of the International Monetary Fund’s (IMF) European Department, issued a similar warning: “The temptation is to simply stop prices from rising, using price caps, universal rebates, or fuel tax cuts. These are unwise measures.”

Progressive Thinking on the Big Issues of Our Time

Read by policymakers, academics and journalists in 100+ countries.

A central charge against price subsidies is that they are ineffective—that they fail to reach consumers because of weak competition in fuel retail markets. Yet the evidence from Germany’s 2022 fuel rebate, the predecessor of the current scheme, is not so damning: roughly 80 per cent of the rebate was passed through to drivers.

There are more fundamental arguments against compensating market-driven price shocks. Above all, one can argue that they reflect genuine scarcities created by supply shocks—the war in Ukraine and the associated sanctions against Russia, the recent closure of the Strait of Hormuz, and now the cascading disruptions of Trump-era trade policy. Compensating price shocks dilutes the price signals that prompt households and firms to cut demand.

But the market price for fuels is only partially determined by the commodity price of oil. It includes various government taxes—above all VAT, an energy tax, and the CO2 tax. The main justification for the carbon tax is the need to reduce CO2 emissions by sharpening price signals. When temporary shocks deliver their own unforeseen price hikes, one can reasonably ask whether an additional incentive from the carbon tax is still required. Germany’s recent fuel discount of 16.7 cents (including VAT) is almost identical to the CO2 tax on petrol. From a climate-policy perspective, then, compensating price shocks by adjusting the carbon tax can be defended.

But is intervention in rising energy prices really necessary at all? The principal justification is that high petrol prices have a negative income effect on private households, particularly those forced to commute long distances. From this angle, one could argue that direct transfers to those most seriously affected would be a better solution than price subsidies.

A different approach to assessing fuel rebates concerns their macroeconomic implications. The main risk of letting energy prices rise without limit is that they affect the whole price system of the economy while simultaneously dampening activity. There is also the risk of second-round effects, in which higher prices feed higher inflation expectations and demands for higher wage increases. Supply shocks therefore confront central banks with a difficult dilemma. If they remain passive, their resolve to fight inflation—and thus their credibility—is questioned. If they raise policy rates, they add to the drag on activity.

Interest rate policy is in any case a very blunt instrument for dealing with higher energy prices and inflation expectations. Its most direct impact falls on the real estate sector, which has little to do with energy demand. It therefore takes time before higher rates show their effect on the price level.

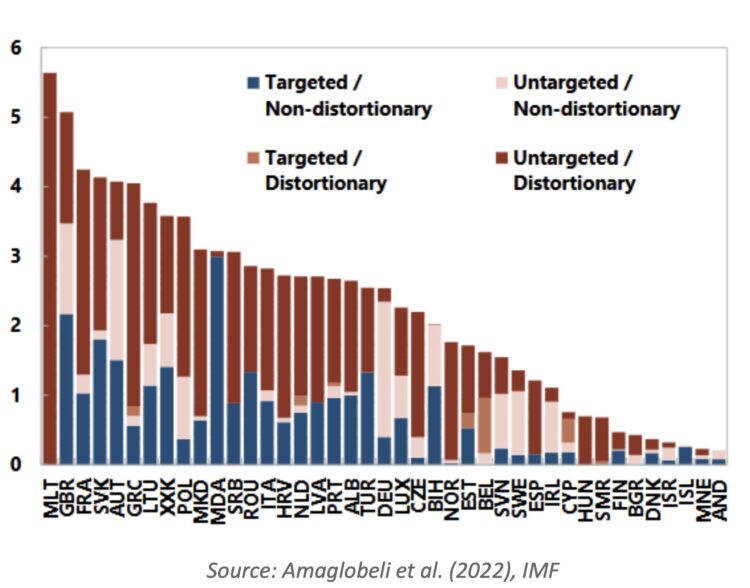

It is precisely this central bank dilemma in the case of price shocks that supplies the macroeconomic rationale for the temporary government compensation of energy prices. During the energy crisis of 2022, many states implemented measures to limit the effect of higher energy prices on the wider economy. As a chart by Amaglobeli et al. (2022) shows, such measures can be divided into “non-distortionary” and “distortionary”—the former being income transfers that have no influence on the price system, the latter interventions that act directly on the prices of particular energy sources, and thus on the inflation rate. On average, countries showed a clear preference for measures with price interventions that benefit all population groups, rather than narrowly targeted ones.

Was this “unconventional fiscal policy” (Gourinchas et al. 2023) successful? In their study, Gourinchas and co-authors conclude:

Overall, we find that these unconventional measures reduced euro area inflation by 1 to 2 percentage points in 2022 and may avoid an undershoot later on. Last, longer-term inflation expectations have remained broadly stable overall, in part reflecting the inflation-suppressing effects of the energy measures. Our estimates suggest that longer-term inflation expectations, as measured by the ECB’s Survey of Professional Forecasters, would have reached 2.5 percent by the end of 2022, 0.3 percentage point higher than the observed 2.2 percent, in the absence of UFP.

They add the caution, however, that “the approach is risky as the temporariness of energy price shocks in real time is difficult to ascertain”.

The outright dismissal of energy subsidies in periods of major price shocks therefore deserves more scrutiny than it usually receives. The macroeconomic case for temporary measures to mitigate the effect of energy prices on overall inflation is strong. Spain’s experience already shows that a comprehensive approach can keep inflation under control. Whether Germany’s Tank-Rabatt will dampen the German rate remains to be seen. But if the present energy crisis persists—and Trump’s tariff politics, combined with continuing instability in the Middle East, give little reason to expect a swift reprieve—a joint European response will be required. Confronted by a US administration that no longer pretends to share Europe’s economic interests, the case for unconventional fiscal policy at the continental level becomes harder for orthodox economists to dismiss.

This article is part of a joint project with the Macroeconomic Policy Institute of the Hans-Boeckler-Stiftung examining Germany’s and Europe’s economic repsonses to the challenges of the second Trump administration.

Help Keep Social Europe Free for Everyone

We believe quality ideas should be accessible to all — no paywalls, no barriers. Your support keeps Social Europe free and independent, funding the thought leadership, opinion, and analysis that sparks real change.

Social Europe Supporter

— €4.75/month

Help sustain free, independent publishing for our global community.

Social Europe Advocate

— €9.50/month

Go further: fuel more ideas and more reach.

Social Europe Champion

— €19/month

Make the biggest impact — help us grow, innovate, and amplify change.